Introduction: What is decentralized finance?

In recent years, the cryptoasset industry has experienced remarkable growth, with a total value of cryptoasset markets peaking at US$2.9 trillion in 2021.1 Cryptoassets were initially created to support a decentralized payment system by using blockchain technology to establish a digital ledger for recording token ownership and transactions. Bitcoin was the first to do this in 2008 and remains the most popular blockchain.

However, the industry has since shifted its focus from providing payments to offering a wide range of financial services. This new set of financial services, known as decentralized finance (DeFi), surged in popularity starting around 2020. They are predominantly offered on a different blockchain—Ethereum.

DeFi operates within a multi-layered structure, as shown in Figure 1. In the bottom (or settlement) layer, the blockchain records and settles transactions. Building on the settlement layer, developers create various cryptoassets, including native tokens (e.g., ETH), stablecoins and non-fungible tokens (NFTs). Ethereum further supports a top (or application) layer that offers financial services such as lending and asset management. Chart 1 shows that since the summer of 2020, the total value of cryptoassets locked into DeFi contracts skyrocketed and then retreated following the collapses of several cryptoasset trading platforms (e.g., Terra, Celsius and FTX) in 2022.

Figure 1: Architecture of decentralized finance

Figure 1: Architecture of decentralized finance

Chart 1: Total value locked in decentralized finance on Ethereum

DeFi is the provision of financial services without relying on traditional intermediaries. The blockchain providing DeFi achieves this by running computer programs known as smart contracts on the blockchain. To understand how a smart contract works, consider the example of collateralized loans such as a mortgage (see Chiu, Kahn and Koeppl [2022] for details). Traditionally, loans between lenders and borrowers rely on a trusted third party (e.g., a bank) that provides custodian services to safeguard collateral pledged as security for a loan. The third party’s incentive to behave properly often depends on external law enforcement as well as the need to maintain a good reputation to stay in business.

Without a trusted party, as in the crypto space, a smart contract acts as the custodian. A borrower locks a digital asset into the contract as collateral, which is released only upon repayment (Figure 2). If the borrower defaults, the smart contract liquidates the collateral to repay the lender. Smart contracts execute automatically based on predetermined conditions. This eliminates the incentive problems that a traditional intermediary might face.

DeFi uses these programmable smart contracts to decentralize a host of financial services, as listed in Table 1. Examples include:

- decentralized stablecoins (e.g., Dai), which facilitate payments

- decentralized exchanges (e.g., Uniswap), which enable asset trading

- lending protocols (e.g., Aave)

- decentralized asset management platforms (e.g., Yearn)

Figure 2: An example of decentralized finance lending

Figure 2: An example of decentralized finance lending

Table 1: Financial services provided by crypto-based finance versus traditional finance

| Service | Traditional finance | Crypto-based finance | |

|---|---|---|---|

| Decentralized finance (DeFi) | Centralized finance (CeFi) | ||

| Funds transfer | Traditional payment platforms | DeFi stablecoins (e.g., DAI) | CeFi stablecoins (e.g., Tether) |

| Asset trading | Exchanges and over-the-counter brokers | Crypto decentralized exchange (e.g., Uniswap) | Crypto centralized exchange (e.g., Binance) |

| Lending | Banks, broker-dealers in repurchase agreements and securities lending | Decentralized crypto lending platforms (e.g., Aave) | Centralized crypto lending platforms (e.g., Celsius) |

| Investment | Investment funds | Decentralized asset management (e.g., Yearn) | Crypto funds (e.g., Grayscale) |

Note: This table is based on S. Aramonte, W. Huang and A. Schrimpf, “DeFi risks and the decentralization illusion,” Bank for International Settlements (BIS) Quarterly Review, December (2021): 21–36.

The market shares of these different sectors of DeFi services are shown in Chart 2, which illustrates the composition of Ethereum’s DeFi system based on the total value of cryptoassets locked into it.

Chart 2: Composition of Ethereum’s decentralized finance services

One important feature of DeFi is its “composability”: because smart contracts are open source, their code can be pieced together like Lego bricks to create new products. For example, one can build on an exchange contract and a lending contract to create a smart contract for margin trading. Composability enables the DeFi system to grow rapidly and increases the amount of interconnectedness across its applications.

Why decentralized finance?

The rise of DeFi was partly motivated by the fact that some transactions in traditional finance are time- and cost-intensive due to inefficient legacy systems and processes as well as monopoly profits earned by incumbents. Cross-border payments, for example, involve multiple currencies and a small number of correspondent banks, resulting in cost and time inefficiencies. Securities settlement also requires reconciliations across multiple ledgers. Proponents believe that DeFi can address these challenges and transform the financial system in three ways:2

- Increased service offering. A unified ledger can reduce frictions in the legacy system and expand the scope of financial services currently being provided.

- Increased competition. Everyone is allowed to enter the crypto space to provide DeFi services and use services offered by others. This characteristic of DeFi can reduce market power and concentration.

- Increased transparency. Replacing intermediaries with smart contracts increases the transparency of the balance sheets and governance of DeFi platforms, thus reducing fraud and custodian risk.

Why not decentralized finance?

Despite its innovations and possibilities, the overall economic benefits of DeFi remain limited. Three key challenges hinder DeFi from realizing its potential:

- Limited tokenization. Only tokenized assets can be recorded on the blockchain and interact with smart contracts. However, few real-world assets have been tokenized thus far, resulting in a self-referential system mainly focused on speculative crypto trades. The contribution to the real-world economy remains minimal.

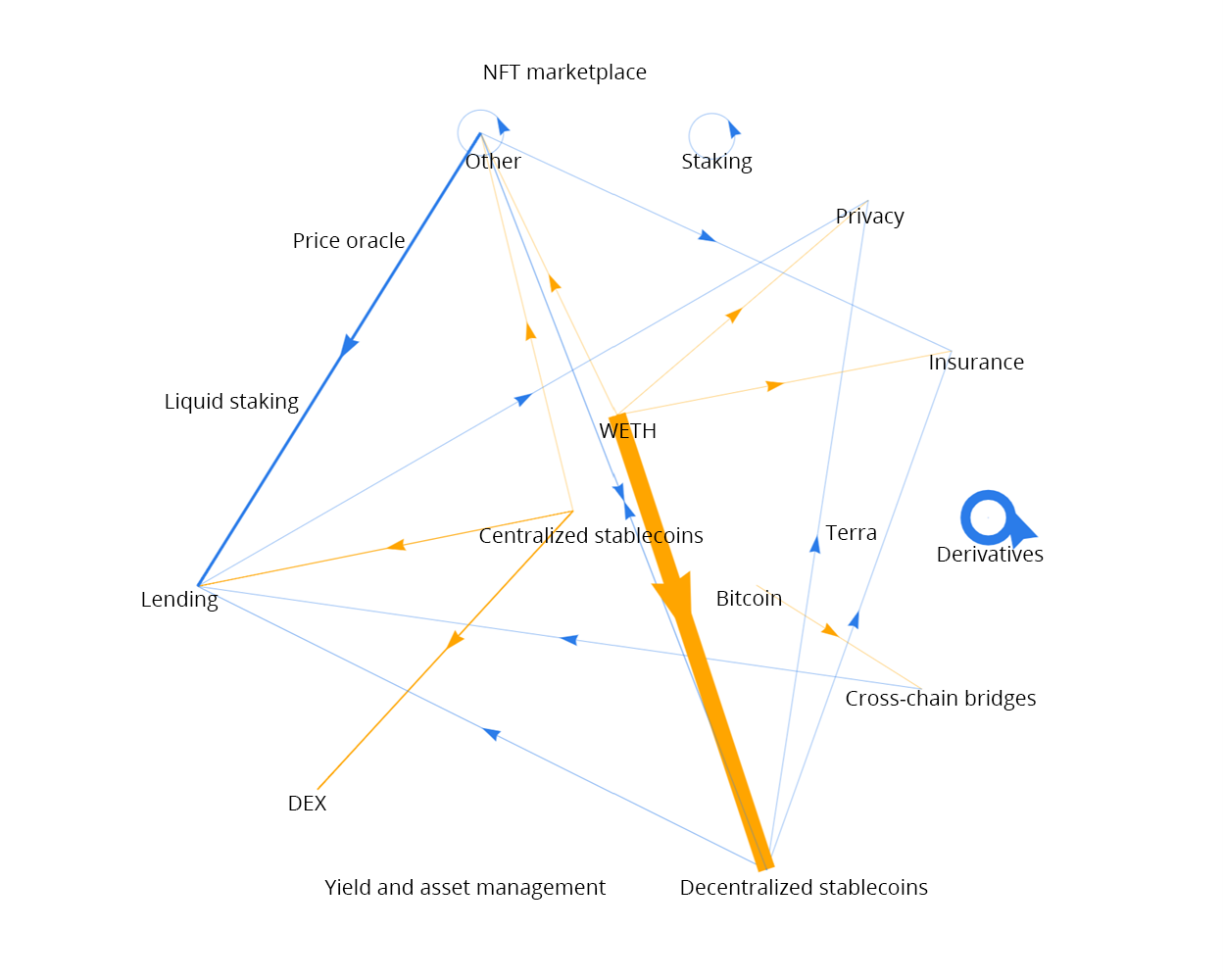

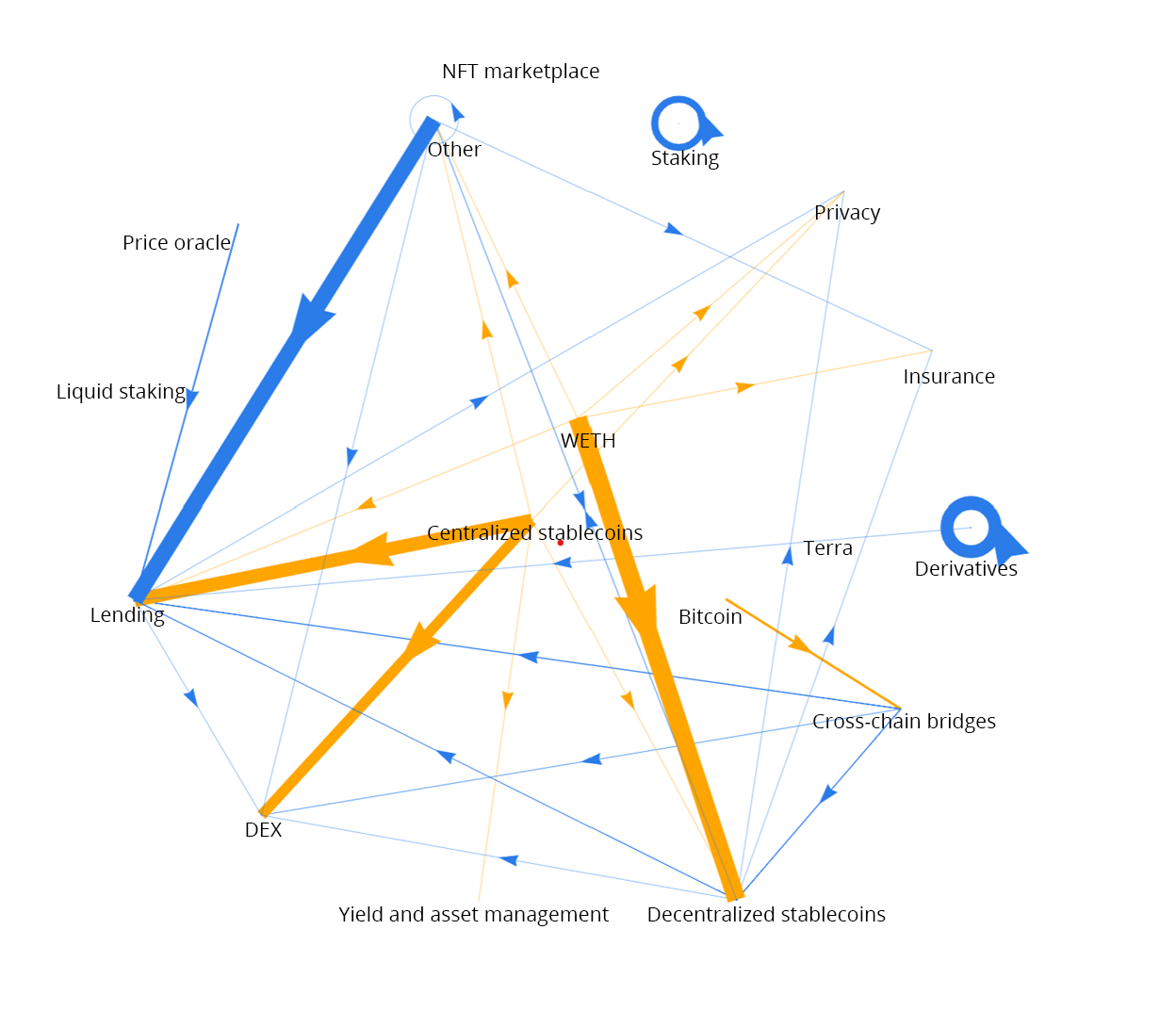

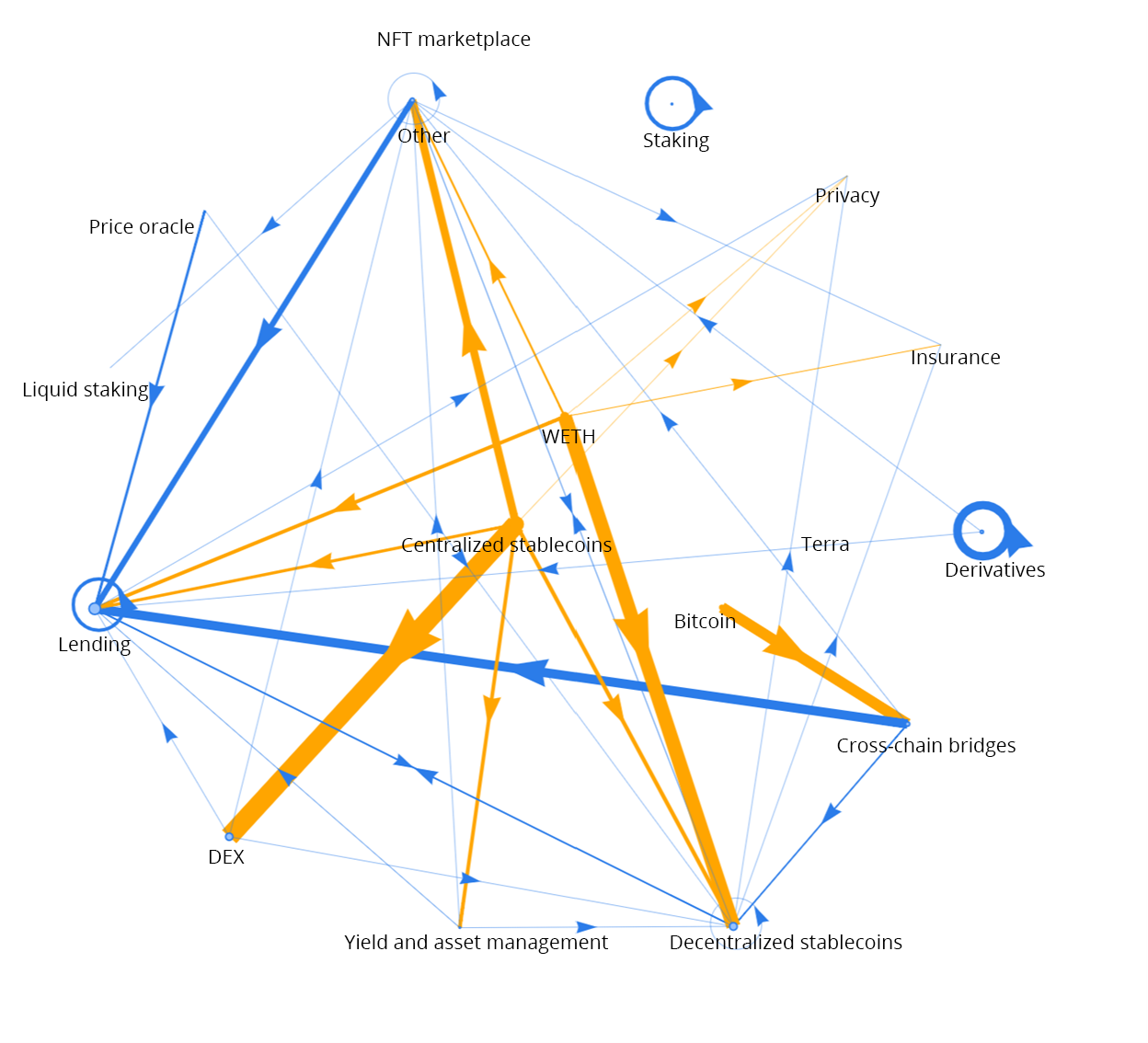

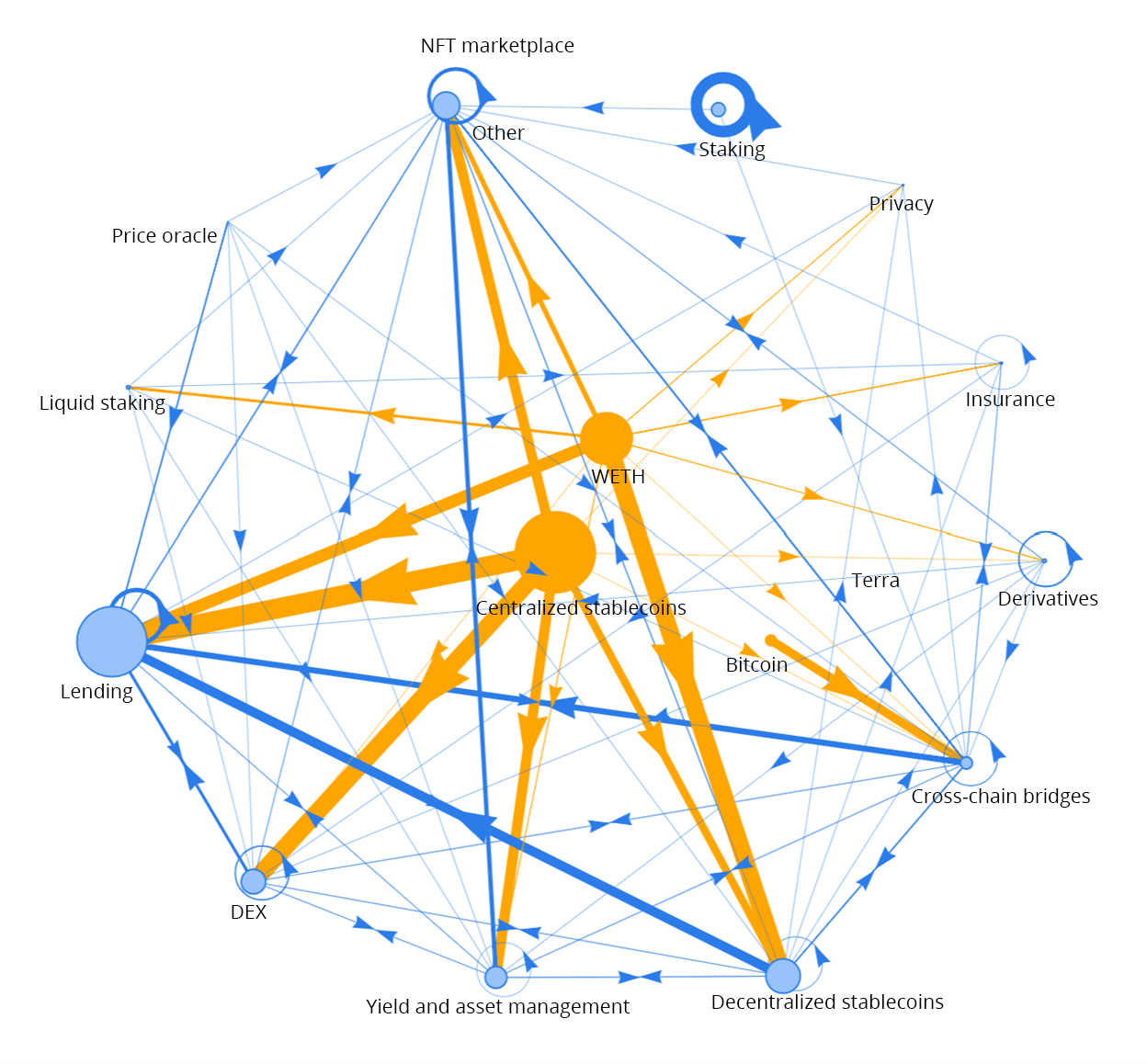

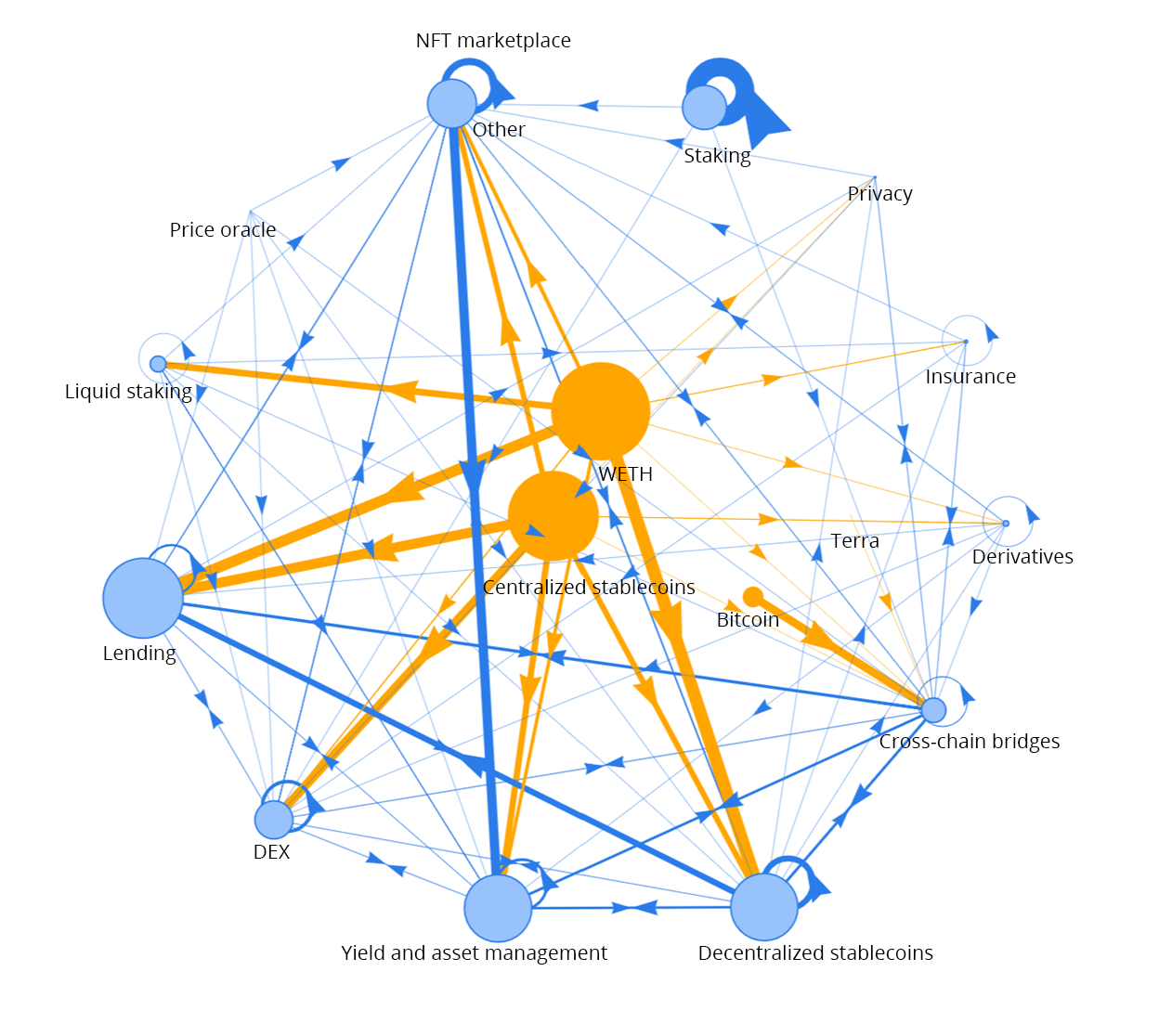

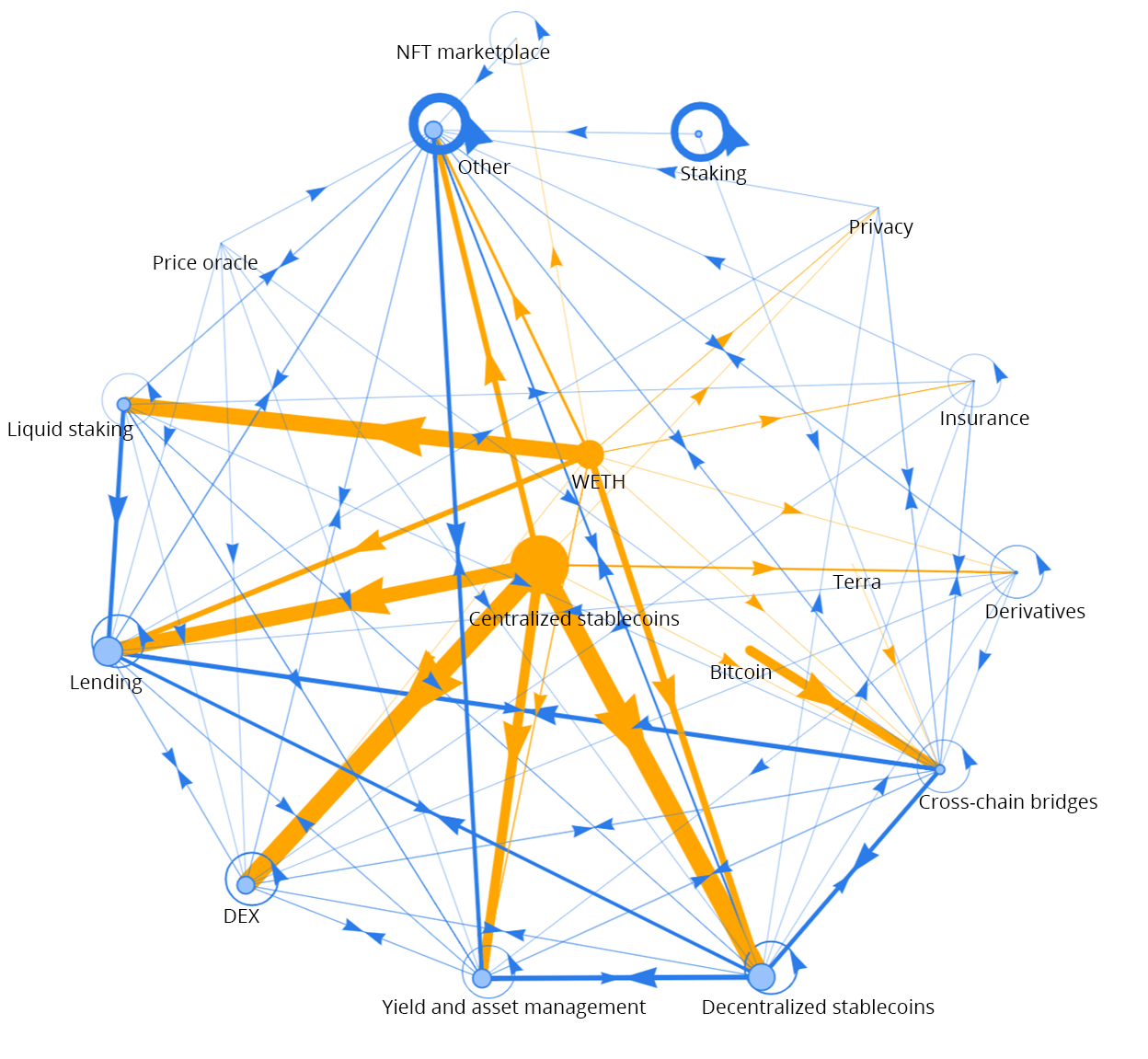

- High concentration and interconnectedness within the system. Figure 3 illustrates the DeFi network on Ethereum, reported by Chiu et al. (2023). As shown, the network has become increasingly interconnected over time. Furthermore, the system relies heavily on the two orange dots at the centre, which represent centralized stablecoins and the native token ETH. The blue dots on the outer circle denote different sectors of DeFi services. While each sector usually consists of multiple service providers, known as protocols, most sectors are rather concentrated because most values are locked into only a few DeFi protocols. Any operational or financial shocks to these key protocols could lead to system-wide spillover effects.3

- Unregulated CeFi. Although DeFi aims to eliminate centralized intermediaries, the specialized knowledge required to manage private keys and interact with the blockchain makes it difficult for retail users to participate in the DeFi system directly. As a result, centralized, non-transparent and unregulated intermediaries called centralized finance (CeFi) have emerged. These CeFi platforms function very differently from their DeFi counterparts. While they also offer financial services using cryptoassets, they differ from DeFi in that they are run by people instead of smart contracts, which exposes investors to custodian risk and lacks transparency. Recent bankruptcies of centralized platforms like Celsius and FTX highlight the risks associated with these unregulated CeFi entities.

Figure 3: Decentralized finance system network in terms of value locked

Figure 3: Decentralized finance system network in terms of value locked

Decentralized finance network

Note: WETH denotes the “wrapped” version of ETH and is a token representing ETH so that it can be used in the DeFi system. DEX is decentralized exchange, NFT is non-fungible token.

Regulatory concerns for decentralized finance

While DeFi currently poses limited risks to financial stability, its connections to the real economy may increase over time. Many vulnerabilities in DeFi mirror those in the traditional financial system, such as run risk with stablecoins, leverage associated with DeFi lending, and interconnectedness among protocols. In addition, DeFi presents new, blockchain-specific challenges, such as:

- new points of failure emerge when the blockchains connect with each other or with the real world (e.g., cross-chain bridges and price oracles)

- new amplification channels such as flash loans allow malicious actors to acquire billions of dollars in funding without any credit checks or collateral requirements

- the anonymous and borderless nature of public blockchains complicates regulatory oversight

Conclusion

DeFi has grown rapidly in scale and scope, forming a complex ecosystem with a high degree of interconnectedness. Its innovative elements, such as smart contracts, composability and tokenization, hold potential for future monetary and payment systems. However, challenges remain, as DeFi introduces new risks to the financial system. Policy-makers and regulators need to strike a balance between promoting innovation and mitigating risk.

Endnotes

- 1. CoinMarketCap, “Total Cryptocurrency Market Cap,” Global Cryptocurrency Charts (September 2023).[←]

- 2. See Chiu and Koeppl (2019) for formal modelling of blockchain-based asset settlement.[←]

- 3. Collateral linkages, for example, can lead to negative spillover effects. In March 2022, the unstable price of the stablecoin USDC had a negative impact on the price of DAI, which used USDC as one of its reserve assets.[←]

References

Aramonte, S., W. Huang and A. Schrimpf. 2021. “DeFi Risks and the Decentralisation Illusion.” Bank for International Settlements (BIS) Quarterly Review (December): 21–36.

Chiu, J. and T. V. Koeppl. 2019. “Blockchain-Based Settlement for Asset Trading.” Review of Financial Studies 32 (5): 1716–1753.

Chiu, J., C. M. Kahn and T. V. Koeppl. 2022. “Grasping Decentralized Finance through the Lens of Economic Theory.” Canadian Journal of Economics / Revue canadienne d'économique 55 (4): 1702–1728.

Chiu, J., T. V. Koeppl, H. Yu and S. Zhang. 2023. “Understanding DeFi through the Lens of a Production-Network Model.” Bank of Canada Staff Working Paper No. 2023-42.

Disclaimer

Bank of Canada staff analytical notes are short articles that focus on topical issues relevant to the current economic and financial context, produced independently from the Bank’s Governing Council. This work may support or challenge prevailing policy orthodoxy. Therefore, the views expressed in this note are solely those of the authors and may differ from official Bank of Canada views. No responsibility for them should be attributed to the Bank.

DOI: https://doi.org/10.34989/san-2023-15