Focusing on the Long Term

Thank you for the invitation to join you this evening. It was exactly a year ago that I met with you in Montréal. It has not been an easy year. All of you have been running companies and making decisions under very uncertain conditions. You have had to deal with corporate and accounting issues. Markets have been volatile. And geopolitical events have shaken confidence.

At times like these, it's easy to get caught up in trying to make one's way through current events that cloud the outlook. But the present uncertainties make it even more important to maintain a focus on strategies that will promote the health of businesses over several years—not just over the next few months or quarters.

The same holds true for economic policy-makers. Failed experiments in previous decades have taught us that, in times of uncertainty, it is extremely important to stick to policies that will foster long-term economic growth.

A longer-term focus

Many of us in this room have reached a stage in life where we have at least two pairs of glasses—one for close-up, and one for distance. We're acutely aware that wearing glasses to focus on something very close makes us lose perspective on things further away. And if we focus only on the here and now, we can lose sight of the future. We need a set of economic bifocals, if you will, to see the impact of current events, as well as the best path to future prosperity.

Tonight, I'd like to speak about that longer-term economic vision. Through more than a decade of macroeconomic reform, we Canadians have created a framework to meet both immediate and longer-term challenges. Even as short-term events have buffeted our economy, we have followed four key long-term policy principles: trade liberalization, structural reform, sound fiscal policy, and low inflation.

Recent Canadian economic performance demonstrates the merit of continuing to set policies with a longer-term view. Short-term adjustments are sometimes unavoidable in the face of extraordinary events—and we've had more than our share of extraordinary events in the past few years! But, on the whole, these basic principles have stood Canada in good stead through the recent difficulties in the world economy. Let me talk about each one in a bit more detail.

Trade Liberalization

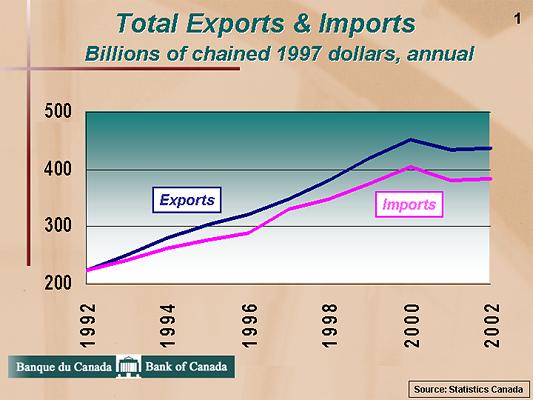

The first principle is trade liberalization, and our economic relationship with the United States has reflected that goal. As you and I discussed last year, the Canadian and U.S. economies made difficult adjustments to freer trade in the early 1990s. The Canada-U.S. Free Trade Agreement and the North American Free Trade Agreement exposed many Canadian companies to stiffer competition. But freer trade also opened up new markets. And Canadian companies have risen to the challenge. Some of the sectors that we used to protect the most—such as furniture, clothing, and wine—have established a strong presence in international markets. On the whole, Canadian industry has flourished with the competitive pressures generated by these agreements. And so has the trading relationship between Canada and the United States.

As you can see from Chart 1, freer trade has clearly meant increased volumes of exports and imports. And now that we have made the adjustment, the more open trading environment is clearly helping to raise living standards for Canadians.

{kind=link}

That should strengthen our resolve to see freer trade extended both within and beyond North America. We need to continue to work towards reduced trade barriers, both within NAFTA and at the Doha round of multilateral talks. It won't be easy, but the long-term economic benefits will make our efforts worthwhile.

Structural Reform

The second principle focuses on improving the structure of national economies, to facilitate adjustment to changing economic conditions and to ensure the longer-term viability of social- and income-security arrangements. A number of initiatives have been undertaken in Canada, but I'm going to focus on only three. I am sure that you're familiar with them, and many of you have participated in the debate surrounding these reforms.

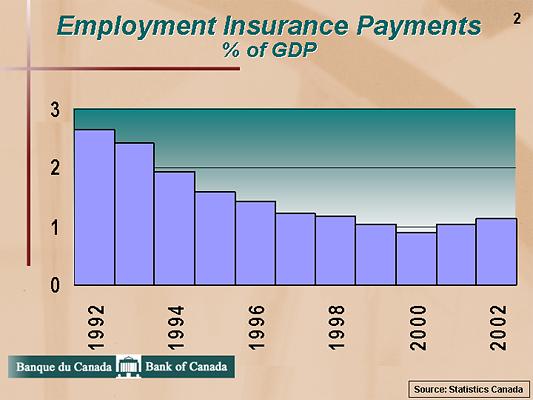

First, Employment Insurance (EI) benefits were restructured to strengthen the incentive to work. With these changes, and with improved economic performance, EI payments as a share of GDP have declined significantly over the past decade, from more than 2 1/2 per cent to just over 1 per cent, as shown in Chart 2.

{kind=link}

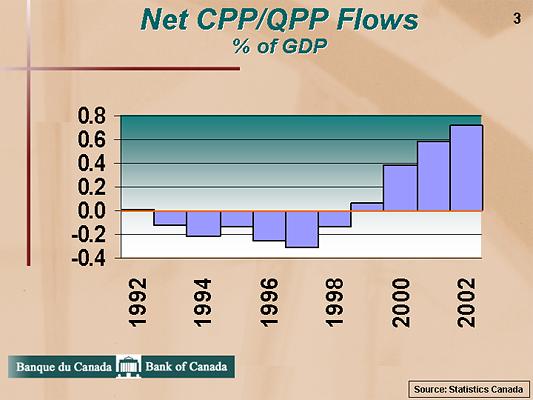

Second, the Canada and Quebec Pension Plans were revamped, to put them on a sustainable footing. The reforms meant some restructuring of benefits and a sharp increase in contributions—moves that were necessary, if unpopular. The results are shown in Chart 3. The assets of the CPP are now managed by the independent Canada Pension Plan Investment Board, the mandate of which is to invest the contributions in markets, in order to generate the best possible returns. These changes mean that Canadians no longer have to worry about the sustainability of their CPP and QPP pensions.

{kind=link}

Third, governments have improved the efficiency of their tax and spending programs. I know that you are familiar with the major federal and provincial efforts to make direct government spending more efficient. Although more work always needs to be done, governments in Canada have also undertaken significant structural changes to our tax regime. They have reduced distortions in the personal income tax system and implemented the goods and services tax to replace the outdated manufacturers sales tax. Structural reform has also included changes to Canada's corporate tax regime—changes that, when completed, will eliminate the federal capital tax and reduce the average statutory corporate tax rate in Canada to a level that is below current U.S. rates.

Of course, there are other structural improvements left to be made. I'm sure many of you have views and suggestions about how to make them. You have been discussing some of them here today. In my view, it is critical that Canada's private and public sectors continue to work together to further improve the structure of our economy and increase our ability to adjust to changing world economic conditions.

Sound Fiscal Policy

Now, the key to good economic performance is sound macroeconomic policy. The Bank of Canada is responsible for monetary policy. But monetary policy operates within a larger macroeconomic context. So, let me start with fiscal policy.

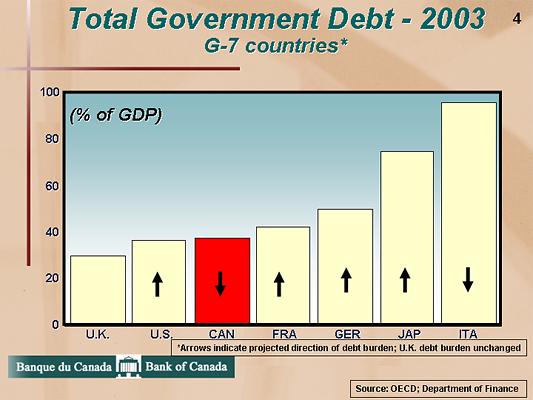

For Canada, the commitment to the principle of sound fiscal policy has meant putting our public debt, as a proportion of GDP, on a sustainable downward track. Many of you remember the difficult and unpopular decisions that had to be taken by federal and provincial governments during the 1990s to achieve this goal.

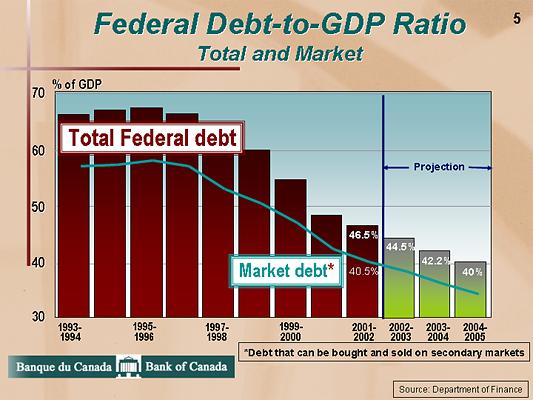

Those efforts are paying off. Today, not only does Canada have one of the lowest debt burdens in the G-7, but, as shown by the arrows in Chart 4, that burden is expected to continue to decline. The federal government has paid down almost $50 billion of its debt—bringing it down from a high of almost 70 per cent of GDP in 1996 to about 45 per cent in 2002, as illustrated in Chart 5. Thus, the vicious circle of rising deficits and debts of the 1970s and 1980s has become a virtuous circle of balanced budgets and falling debt.

{kind=link}

{kind=link}

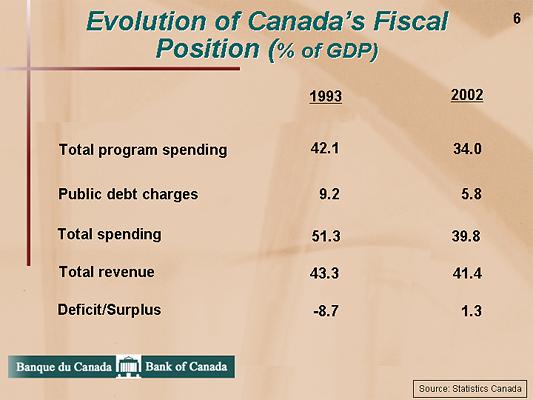

Program spending for all levels of government has dropped from 42 per cent of GDP in 1993 to 34 per cent last year, as you can see in the table. And debt-servicing costs have dropped from about 9 per cent of GDP to less than 6 per cent.

{kind=link}

Here's how Finance Minister Manley summed up this principle of fiscal discipline in his February budget speech: "Keeping a balanced budget, cutting debt and getting the best value for money are a constant challenge and a constant imperative. These are the bedrock of our fiscal and economic strategy."

Low Inflation

Complementing a sound fiscal policy is a monetary policy focused on keeping inflation low and stable—that's the fourth principle, and that is the Bank of Canada's responsibility. Canada's inflation-targeting framework works in a symmetrical way to keep consumer price inflation at the 2 per cent midpoint of a 1 to 3 per cent range. If the trend of inflation moves away from the target, in either direction, the Bank will take action to return it to the target within 18 to 24 months.

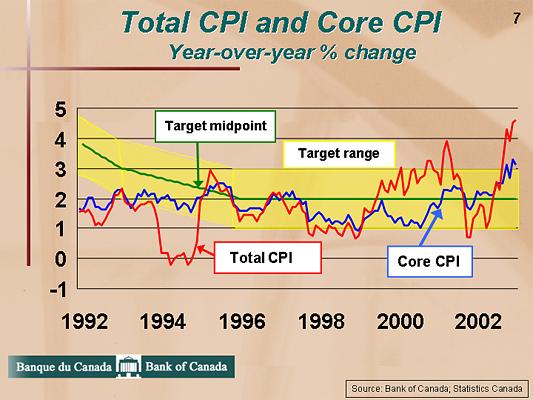

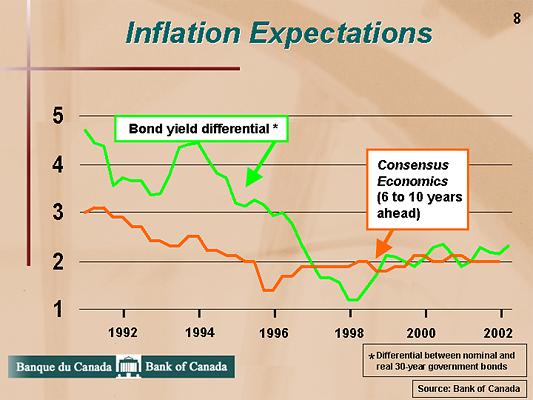

Through most of the past decade, we have managed to keep inflation around the 2 per cent target midpoint, as you can see in Chart 6. As a result, Canadians' expectations for inflation have become firmly anchored around 2 per cent, as shown in Chart 7. That is extremely valuable for decision-makers in business, government, and households. This climate of low, stable, and predictable inflation has helped to smooth out the ups and downs in the economy and to create the best possible environment for longer-term economic growth in Canada.

{kind=link}

{kind=link}

Let me now spend a few minutes describing the circumstances in which monetary policy is currently operating. Even though growth slowed in the fourth quarter of 2002, reflecting global economic and geopolitical uncertainties, our economy continues to operate close to capacity.

As we said in our January Monetary Policy Report Update, a number of indicators support this view. They include high industrial-capacity utilization; a record-high labour force participation rate; a record-high employment-to-population ratio; corporate profits at their highest level since early 2001; and trend inflation that is running above target.

Canada's inflation numbers continue to reflect the impact of higher-than-expected prices for crude oil and natural gas, further increases in auto insurance premiums, and price pressures in certain sectors, such as housing, food, and some services. This higher inflation also suggests an underlying firmness in the price-setting environment. Relative price increases wouldn't be pushing up trend inflation if there was not sufficient demand.

So, in making our latest interest rate decision on 4 March, we weighed not only domestic inflation pressures and the expectation that Canadian economic activity will remain near potential in 2003, but also the stimulative stance of monetary policy and improved conditions in capital markets. Taking these factors into account, we raised our key policy rate by one-quarter of a percentage point to 3 per cent.

Even with this increase, the stance of monetary policy in Canada remains stimulative. Thus, over time, further reductions in monetary stimulus will be required to return inflation to the target in the medium term. But, as we have said, the timing and pace of increases in policy interest rates will continue to depend on a number of considerations. These include: the strength of demand pressures; the evolution of inflation expectations; the impact on confidence of global economic uncertainties; and the way in which the war in Iraq affects demand and inflation, both globally and in Canada. The Bank continues to monitor all of these factors and will adjust monetary conditions to keep Canadian inflation low, stable, and predictable over the medium term. The Bank's next Monetary Policy Report, to be released on 23 April, will provide a full update of our assessment of the economy and of the outlook for inflation.

Conclusion

In closing, let me repeat that, in these trying times, it is tough indeed to maintain a clear view of the current economic picture. But, if we spend all our energy focusing on the near term, we risk losing sight of what's farther out. Your job is to build enterprises that will flourish over the longer term. And our job as policy-makers, whether on the monetary or fiscal side, is to create the best possible climate for sustained economic growth. In an uncertain world, the best thing we can do is to stick to sound economic policy principles. They have proven to be the most effective tools to deal with short-term turbulence and, at the same time, promote solid, sustainable economic growth and prosperity over the longer term.