The Conduct of Monetary Policy: Dealing with Changes in the Terms of Trade

Good evening. I'm delighted to be here in Kelowna, in the beautiful Okanagan Valley.

It's good to be back in a classroom, speaking to business and economics students. For those of you who want to work in finance or the wider world of business, it is particularly important that you have a solid grasp of economic issues and that you understand how monetary policy contributes to the economic and financial well-being of Canadians. And as you will find out, economics is a way of thinking, one that combines logic and pragmatism. The more you know about basic economic concepts, the better you'll perform in whatever career you choose.

What I would like to do in the next 20 to 30 minutes is explain how monetary policy helps the economy adjust to important shocks that occur from time to time, including sharp movements in our terms of trade. I will start with the objective of monetary policy. Then I'll describe how monetary policy works and where the exchange rate fits in. I will then explain what we mean by "terms-of-trade" shocks and show how Canada's monetary policy framework helps to facilitate the adjustment to these shocks. I'll leave plenty of time at the end of my remarks for questions.

Let me start with the objective of monetary policy.

The Objective of Monetary Policy

The ultimate goal of Canadian monetary policy is to help our economy achieve its maximum sustainable growth, and thus contribute to rising living standards for Canadians. The best way to achieve this goal, we've learned from experience, is to keep inflation low, stable, and predictable.

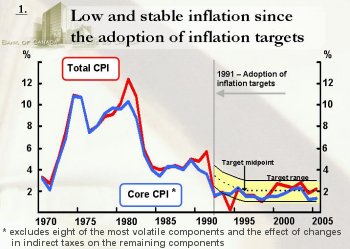

Inflation, as measured by the annual rate of increase in the consumer price index (CPI), has been running at about 2 per cent for more than a decade now. But in the 1970s and 80s, the rate of price increases was a good deal higher, spiking twice to well over 10 per cent (Chart 1). I doubt that many of you here tonight remember those days of high and variable inflation. High inflation exacted a heavy toll on Canadians. Borrowers faced high and volatile interest rates. Incomes and savings were eroded by rising prices. Speculation was rampant. And the economic booms that led to rising inflation ended up in recessions.

{kind=link}

One of the things we learned from this bitter experience is that high inflation injects additional uncertainty into decision making. In a market economy, prices contain valuable information. When the price of a product is rising relative to other products, it's a signal that that particular product is becoming scarcer. Producers are then encouraged to increase its supply, while consumers are encouraged to economize on its use, thus alleviating the scarcity. Conversely, a drop in the price of a product is a signal that it is becoming more abundant. When this happens, firms are led to reduce their supplies of the product, and consumers are encouraged to increase their demand for it.

But when inflation is high and variable, buyers and sellers are never quite sure what a price increase means. Is it a sign that a specific good is becoming scarcer, or is it just a sign of more widespread inflation? This uncertainty means that prices no longer convey as much useful information, and, as a result, people find it difficult to make sound decisions about production and investment. They focus on trying to protect themselves against the effects of inflation. Investors won't commit their resources for lengthy periods; labour negotiations become more acrimonious; and the overall economy is not as productive as it could be. Indeed, with the erosion of confidence in money comes an erosion of confidence in the fairness of markets. As former Bank of Canada Governor Gerald Bouey aptly put it in his 1981 Annual Report, "inflation melts the glue that holds free societies together."

The lesson we (and other central banks) have learned in the past 30 years is that low and stable inflation is the best contribution that monetary policy can make to a strong economy. Since 1991, the Bank of Canada has conducted monetary policy with an explicit numeric target for inflation, a target that is set jointly with the Government of Canada. Since 1995, the inflation target has been the 2 per cent midpoint of a 1 to 3 per cent range. It was last renewed 5 years ago, and is coming up for renewal this year.

Having a clear objective has increased the Bank of Canada's accountability to Canadians. It has made it easier for the Bank to explain its actions and easier for people to judge how the Bank is doing in meeting its objective. Once Canadians believed that the Bank would take action to meet the target—as we have done for some 15 years—they came to expect that inflation would remain low and stable. This expectation helped people make economic decisions that are aligned with the objective of monetary policy. And this facilitates the achievement of that objective.

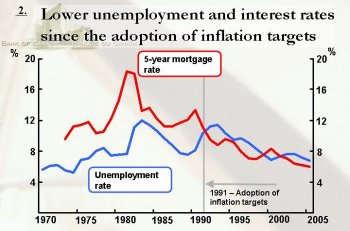

Since the adoption of the target, inflation has been pretty close to 2 per cent. And this stable, low-inflation environment has produced steadier economic growth, as well as lower and more stable interest rates, than was the case when inflation was high and variable (Chart 2).

{kind=link}

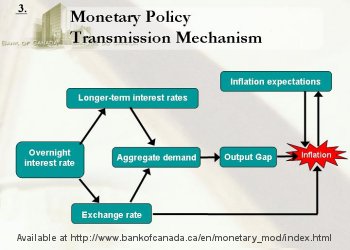

Now that I have described the objective of monetary policy, let me turn to how we go about achieving it. I will start with what we call the "monetary policy transmission mechanism," which traces how monetary policy actions work their way through the economy (Chart 3).

{kind=link}

How Monetary Policy Works

The Bank of Canada has only one tool at its disposal for carrying out monetary policy—its direct influence on the overnight rate. The overnight rate is the interest rate at which financial institutions borrow and lend one-day (or overnight) funds among themselves. The Bank has a direct influence on that rate because it controls the total amount of funds (settlement balances) available to these institutions. 1 The Bank sets the target for the overnight rate eight times a year on a pre-announced schedule. That schedule reduces uncertainty in financial markets about the timing of policy actions and helps direct attention to the medium-term perspective of monetary policy. The decisions are made by the Bank's Governing Council—that is the Governor and five Deputy Governors—based on consensus. They are informed by a thorough analysis, provided by Bank staff, of current and prospective economic and financial developments.

Changes in the target for the overnight rate spread to other interest rates, which then affect borrowing and spending decisions, and thus the overall level of demand for goods and services—what we call aggregate demand. Imbalances between aggregate demand and the economy's capacity to supply goods and services (referred to as the output gap) set off changes in inflation. That's a quick sketch of the transmission mechanism, and I would encourage you to look up a fuller description on our web site at: www.bankofcanada.ca/en/monetary_mod/index.html.

My key point here is that the whole process takes time. Monetary policy actions take 12 to 18 months to have most of their effects on total spending, and another 3 to 6 months to have most of their effects on inflation. This means that the Bank of Canada has to be forward-looking, taking actions based on projections of future pressures on inflation.

Monetary policy aims to keep inflation low and stable by keeping overall demand in line with supply. When demand is projected to rise beyond the economy's ability to meet that demand, threatening to push inflation above target, the Bank will act to dampen some of that demand by raising interest rates. Conversely, when demand is weak, threatening to take inflation below target, the Bank will lower interest rates to stimulate demand. This symmetric, forward-looking approach to monetary policy has a stabilizing influence on the economy, thus helping to prevent costly boom-and-bust cycles. If we waited for inflation to increase or decrease before tightening or loosening monetary policy, we would be too late, and there would be a risk that the economy would be less stable.

The Role of the Exchange Rate

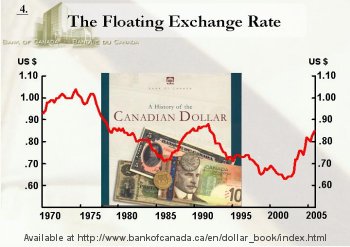

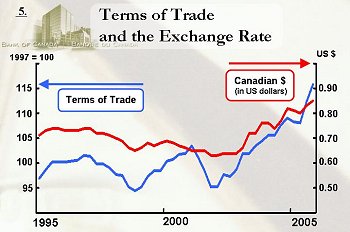

Except for a brief period from 1962 to 1970, when the exchange rate was fixed, Canada has had a floating exchange rate since 1950. 2 Today, the Canadian dollar is worth about 86 U.S. cents. Four years ago, it was worth 63 U.S. cents (Chart 4).

{kind=link}

Our flexible exchange rate regime is an essential ingredient of our inflation-targeting system. It allows us to follow an independent monetary policy, suited to our own economic circumstances, which would not be possible if we had to set monetary policy with the objective of maintaining a fixed exchange rate for the Canadian dollar. At the same time, inflation targeting means that our floating exchange rate acts as a "shock absorber," helping our economy adjust to changes with less pain and less disruption than if the exchange rate was fixed.

So, we do not have a target for the external value of the Canadian dollar. With only one instrument—the target for the overnight rate—to carry out monetary policy, we couldn't hit two targets, one for inflation and one for the exchange rate. But saying that we do not have a target for the exchange rate doesn't mean that we ignore it. On the contrary, we monitor the exchange rate closely to assess the effects of currency movements on aggregate demand for Canadian goods and services, and the consequences for future inflation. The fact is that the exchange rate is an important price in the Canadian economy. It directly affects the Canadian dollar price of everything we import and export, thus sending strong price signals to businesses and consumers.

Terms-of-Trade Shocks and the Flexible Exchange Rate

As an open economy and a major producer of commodities, Canada is very much affected by swings in the world demand for, and prices of, our products. Such swings cause our terms of trade—that is, the prices we get for our exports relative to the prices we pay for our imports—to move around a great deal. When the prices of the products we sell on world markets rise relative to the prices of those we buy from abroad, our terms of trade are improving—and we are getting richer. When the prices of our exports fall relative to those of our imports, our terms of trade deteriorate—and we are getting poorer.

So, improving terms of trade are favourable for a country. They result in gains in labour income, in corporate profits, and in government revenues. But changes in our terms of trade—whether in a favourable or unfavourable direction—can cause stress and dislocations. They can involve significant shifts in production and employment among sectors of the economy. That means loss of jobs in some industries and growth in others. In economic terms, it triggers a shift of resources from less profitable to more profitable sectors. Thus, while the adjustments can be difficult, they are vital to our economic prosperity. To make the most of our opportunities as a trading nation, we need to adjust to changing global economic circumstances.

The key point I would like to emphasize here is that our low-inflation target and our flexible exchange rate help facilitate the necessary adjustments. Of course, by its very nature, monetary policy is national in scope, and while its effects are far-reaching, it cannot address the specific needs of a sector or region. It can only address the needs of the nation as a whole.

Canada's terms of trade have moved around significantly over the past decade (Chart 5). To illustrate my point, I'd like to focus on one episode when they were weakening and one when they were improving. I'll describe the nature of the shock in each case, and explain the role of our monetary policy framework, in particular, the role of the exchange rate, in facilitating the adjustment process.

{kind=link}

The first episode occurred in 1997-98, when a financial crisis that started in Thailand spread to Indonesia, South Korea, and other countries. Asian demand, which had accounted for a relatively large share of growing world demand for commodities, weakened considerably. As a result, prices of key commodities produced by Canada fell, and our terms of trade weakened.

Reflecting the downturn in world commodity prices, the Canadian dollar depreciated against the U.S. dollar. The depreciation helped to mitigate the negative shock for commodity producers. And, more importantly, it encouraged the manufacturing sector to expand and absorb the resources—labour and capital—that were released from the commodity-producing sector. Thus, the depreciation of our currency helped to offset the negative effects of the Asian crisis on aggregate demand for Canadian goods and services and thus pre-empted downward pressures on prices and wages. In this way, the flexible exchange rate acted as a shock absorber to mitigate the effects of the weakening terms of trade on the overall level of economic activity, while encouraging economic adjustment.

Let me now turn to the second episode. In the past three to four years, Canada's terms of trade have improved sharply. The basic story has been one of strong global economic growth, leading to a surge in world demand and prices for oil and gas, lumber, metals, and other primary commodities. The resulting rise in Canadian incomes has also boosted demand by Canadian households and businesses.

Over this period, the Canadian dollar has appreciated by more than 30 per cent against the U.S. greenback, and indeed significantly against many other currencies. This stronger Canadian dollar has dampened the positive shock for commodity producers and made manufacturing less competitive. As a result, resources have been reallocated from the manufacturing sector to the commodity and services sectors. This adjustment has helped keep overall supply and demand in balance and inflation pressures in check. In this sense, the past four years have been the reverse of the situation in 1997-98. Once again, the flexible exchange rate has helped to stabilize the economy and to encourage adjustment—this time in the context of strengthening terms of trade.

It's useful to compare these two recent terms-of-trade shocks—which occurred when monetary policy was anchored by an inflation target—with an earlier shock when monetary policy was not conducted with an explicit target. During 1997-98, when our terms of trade were weakening, CPI inflation averaged 1.3 per cent. Since the beginning of 2003, when our terms of trade have been strengthening, inflation has averaged 2.6 per cent. Thus, during both of these recent episodes, inflation has remained relatively close to target.

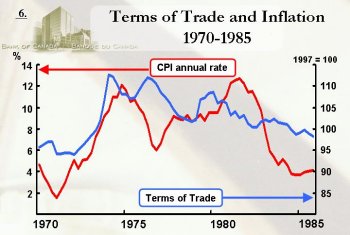

This is in sharp contrast to the 1972-74 period, when Canadian terms of trade improved dramatically as a result of steep increases in energy and other commodity prices (Chart 6). Inflation rose sharply, spiking to more than 12 per cent in late 1974. Inflation remained high and variable for quite some time after that, causing severe economic disruptions, and great difficulty for people living on fixed incomes. Clearly, the monetary policy framework at the time was not robust enough to contain the inflationary consequences of rising energy and raw material prices and strong demand for commodities.

{kind=link}

The comparison of these episodes illustrates how the two key elements of our current monetary policy framework—the inflation-control target and the flexible exchange rate—work together to facilitate the adjustment to terms-of-trade shocks.

To summarize: sharp changes in the terms of trade necessitate a reallocation of economic resources. That adjustment process, while always a challenge, and sometimes painful, can be helped a great deal by a coherent monetary policy framework. Of course, monetary policy is only one part—albeit an important part—of the adjustment process. Also of great help in facilitating economic adjustment to terms-of-trade shocks are the ingenuity of Canadian business people, the diversity and resilience of the Canadian economy, and the flexibility of labour and product markets.

Over the past three years, we've seen strong growth in capital spending in commodity-producing industries, as well as substantial gains in both capital spending and employment in sectors with low exposure to international trade. Exports have continued to grow, despite the higher Canadian dollar. And a surge in investment in machinery and equipment suggests that firms are, in fact, taking advantage of the stronger exchange rate (which reduces the cost of imported machinery and equipment in Canadian dollar terms) to improve their productivity and enhance their competitiveness.

There is also evidence that Canadians are more mobile, making the best of work opportunities in strong growth areas such as the Athabasca tar sands. Indeed, it has recently been reported that Air Canada is introducing an "Oil Express" pass to facilitate the movement of labour between Eastern Canada and Fort McMurray, Alberta. And strong economic activity in Alberta is not only drawing in migrant labour from other provinces; it is also generating large orders for goods and services produced elsewhere in Canada.

Here in British Columbia, there has been solid growth in output in the construction, mining, transportation, and the services sectors. Indeed, B.C. now enjoys its lowest recorded unemployment rate. A Vancouver firm recently signed the largest licensing deal in Canada's biotech history.

In B.C. and across Canada, workers and investors have been quick to seize the new opportunities presented by the improvement in our terms of trade.

Recent Economic Developments

The global economic environment has been particularly favourable to Canada in the past few years, and our economy has adjusted remarkably well to large changes in relative prices, including the marked appreciation of the Canadian dollar.

In our January 2006 Monetary Policy Report Update, we concluded that the Canadian economy was operating at its production capacity and we projected that it would grow roughly in line with capacity through 2007. We expected CPI inflation to stay slightly above the 2 per cent target in the first half of this year and to ease to 2 per cent by the first half of next year. Core inflation—a measure of the underlying trend in prices that excludes eight of the most volatile components of the CPI, and which has been slightly below 2 per cent in the past two years—was also projected to return to 2 per cent by the first half of next year.

Our January Update also indicated that the risks to the Bank's projection were balanced for 2006, but tilted to the downside through 2007 and beyond. These downside risks relate to the possibility that the unwinding of large global current account imbalances could involve a slowdown in the world economy. (By global imbalances, I mean the large current account deficit in the United States, mirrored by large current account surpluses in other countries.) Consistent with this view, at the time of our last policy decision on 7 March, we indicated that some modest further increase in the policy interest rate may be required to keep aggregate supply and demand in balance and inflation on target over the medium term.

We are now well into the preparation of our spring Monetary Policy Report, which will be released on 27 April. If anything, the global economy may be a touch stronger in 2006 because of improved growth prospects for Japan and Europe. In our upcoming Report, we will provide a full analysis of economic developments, trends, and risks to the outlook.

Conclusion

Let me conclude. In a constantly changing and increasingly globalized world economy, the Canadian economy will continue to be buffeted by various shocks. Our monetary policy framework—the inflation target working in concert with a floating exchange rate—will continue to play an important role in mitigating the effects of shocks, and in helping to facilitate the needed economic adjustments by ensuring that the price system sends the right signals.

And of course, the ingenuity and adaptability of Canadian workers and business people will remain critical to increasing our standards of living.

This is an exciting time to be in post-secondary education, preparing for a career in Canada. Employment prospects are very good, and they will undoubtedly improve as the baby boomers retire. I talked about the inevitability of economic shocks and of the adjustments that these shocks necessitate. You will find that your studies will help you to prepare for, and to take advantage of, rapid changes in our economy. I wish you all well in your studies.